Digital era banking systems revisited

In our blog of 2019 on digital era banking systems, we argued that technology, regulatory and other trends were breaking up the historically monolithic financial services value chain and forcing an architectural change in banking systems — and we predicted the proliferation of “systems of intelligence”.

Nearly 6 years on, we believe it’s time to revisit our original post: 1/ to ask ourselves whether the theory is playing out as we had expected and 2/ with the advent of Generative AI, which is reducing the cost of “intelligence” and making it accessible to everyone, to ask whether systems of intelligence are still as relevant as we thought.

The short answer is yes.

Firstly, while adoption of systems of intelligence has been slower than we anticipated, we argue that this is because financial institutions have been able to defer action, but the window on procrastination is shrinking. The arrival of GenAI is one of the factors that will actually galvanize change.

Secondly, even though GenAI marks an inflection point, it forms part of a continued evolution of computing and networks, rather than a paradigm shift. By commoditizing and enabling AI capabilities, it makes adjacent parts of the value chain correspondingly more valuable, such as proprietary data and orchestration. Deploying systems of intelligence will be critical, therefore, if incumbent financial institutions are to benefit from this value shift.

The system of intelligence thesis

Most banks still run on branch-based accounting systems that they have modified and augmented over time as their businesses evolved. That is to say, there has not been any major change to system architecture for decades.

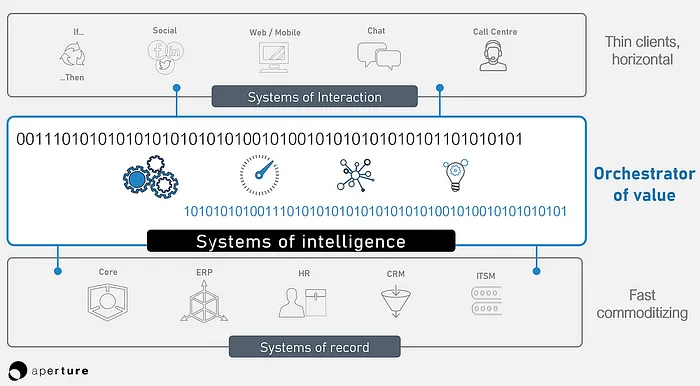

In our original post, we argued that this was unsustainable and financial institutions would need to introduce a new architectural layer, a system of intelligence, to mediate between customer channels (systems of interaction) and their book-keeping systems (systems of record).

Our argument was mostly about scalability, but also user experience and business models.

A scalability challenge

On scalability, we suggested that systems of record were not architected for, and would not cope with, the explosion in the look-to-book ratio that was occurring as customers — directly and indirectly — continuously queried their financial information. Since the most important systems of record were designed for a branch-based world, they are not equipped for 24/7 and real-time banking. For example, most branch-based accounting systems make no distinction between a transaction (e.g. a cash withdrawal) or an interaction (e.g. a balance enquiry).

As a result, we argued that a system of intelligence would be necessary to sit between interaction channels and systems of records to introduce more scalability. For instance, the system of intelligence would be able to distinguish between interactions and transactions, fetching cached data to answer queries and only writing new information to the system of record in the case of transactions. We drew precedents from other industries, such as retail, where order entry is handled asynchronously from order fulfilment (Amazon thanks you for your order before emailing you the confirmation and in between it sends information to the warehouse system to pick the order and to the accounting system to bill you).

A user experience challenge

On user experience, we argued that to deliver truly rich and seamless experience across multiple channels, financial institutions would need to draw insight from multiple systems of record (e.g. information about your investments from the portfolio management system about your age and risk profile from the CRM system) as well as other information sources (e.g. contextual information about your channel preferences or market information about interest rate outlook).

Furthermore, we asserted that this information aggregation could not be done either by the system of record (because it needs to aggregate information from multiple systems of record) or by the system of interaction. In the case of the system of interaction, we argued that these were changing too quickly to hold critical logic, that putting too much logic into one system of interaction over another would undermine the “omnichannel experience” and because we foresaw that financial services would be increasingly distributed via other financial and non-financial distribution channels (embedded finance).

Therefore, we argued that a system of intelligence would be needed also to solve the customer experience challenge.

What has happened since

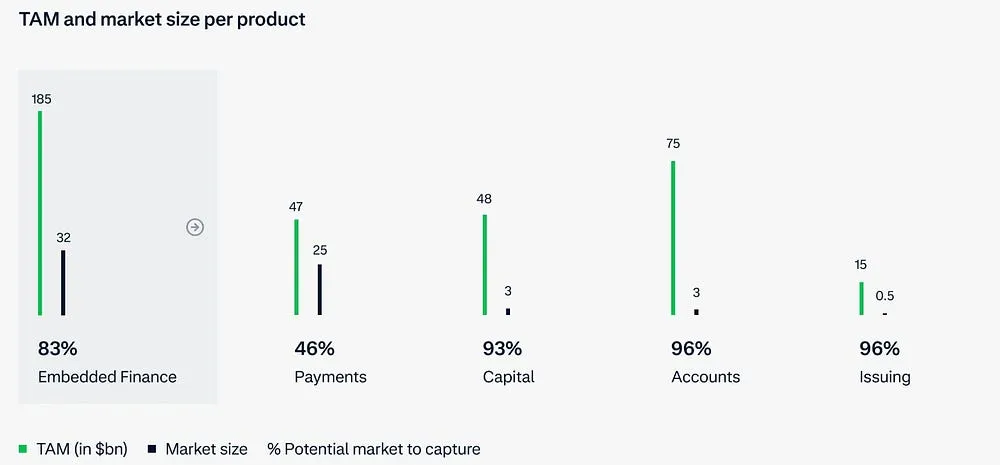

Embedded finance has continued to grow in importance. Arguably, we have been through a hype cycle, reaching peak excitement in 2021 and hitting the trough of disillusionment 2023. But embedded finance has continued to expand. According to analysis from Matt Brown, 83% of Vertical SaaS companies embed payments into their application, while analysis from Ayden puts the value of the embedded finance opportunity in Europe and North America at USD185bn. The premise of adapting financial services to context and providing them at the point of need is too compelling to slow this secular growth opportunity.

Embedded finance puts more pressure on system architecture. Branch-based accounting systems not only assumed in-person transactions during working hours, but they also assumed a financial institution would be selling exclusively its own products.

Against the challenges of scalability and user experience, financial institutions also face the challenge of how to open up their sourcing models to external product manufacturers and how to open up their distribution models to allow for distribution through third-party distribution channels. For instance, if order capture is not distinct from order entry, this is not only a scalability issue but a business model issue in that it does not allow for orders to be originated through third-party channels. Another missing element would be a product catalogue that incorporates inventory from third-parties, which could not be added to a system of record (because it needs to interface to multiple systems of record, internal and external) and could not be added to the system of interaction because orders could be originated through multiple systems of interaction, internal and external.

Suffice it to say that a system of intelligence will also be needed for financial institutions to embrace the structural trend towards embedded finance.

Capitalizing on GenAI, another structural shift, will also necessitate system architecture changes.

GenAI will change systems of interaction

With the advent of GenAI, we see new interaction channels, faster replacement cycles, as well as UIs disappearing altogether.

Firstly, we are seeing new interaction channels. New intelligent agents and “wrappers” are emerging to help us to streamline everything from note-taking to managing our health. These channels will proliferate, both for consumers and for enterprise users.

Second, we are seeing faster replacement cycles. GenAI is making it much cheaper and quicker to develop software and this will translate into faster release cycles across many areas, but especially customer interaction channels.

Third, we have all experienced the ease and convenience of conversing in a human-like way with GenAI tools like ChatGPT. Financial institutions will soon open up the same natural language interfaces to consumers and business users to deliver a more customised experience. .

All in all, this reinforces our view that it is flawed to try to put too much logic into systems of interaction given this changing landscape and underlines the need for a separate system of intelligence.

Systems of record remain fundamental, but require orchestration

As with any important new technology, GenAI changes how value is created and distributed across a value chain.

In lowering the cost of intelligence, GenAI reduces the need and value of having standalone business intelligence applications, for example. But proprietary data becomes more important and, as a result, the systems that hold these — systems of record — remain fundamental. Moreover, financial institutions need to continue to upgrade these systems, moving to cloud-native, API-first systems like Tuum (for retail and corporate banks) and Light Frame (for private banking) if they are to be able to leverage effectively their data assets.

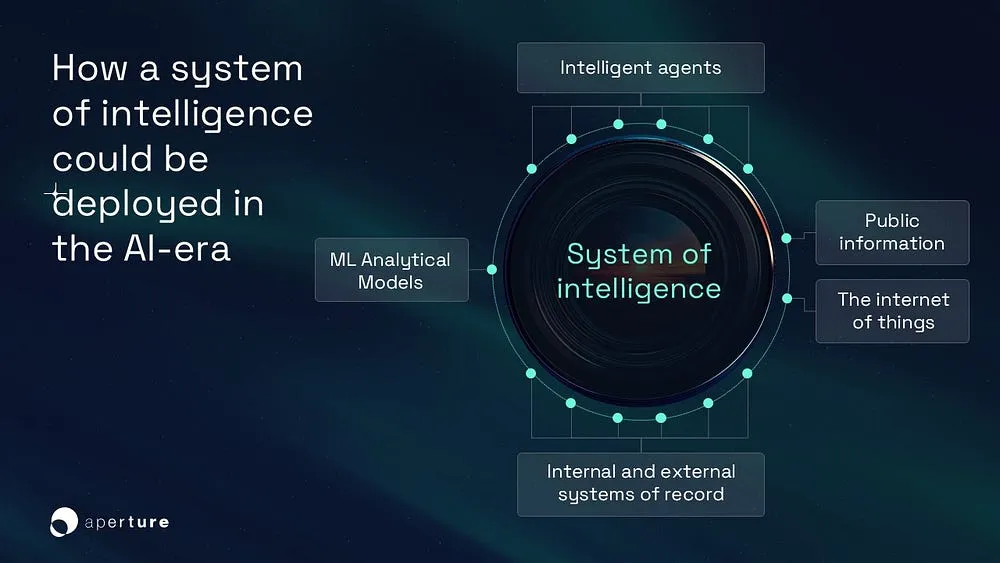

But systems of record require orchestration through systems of intelligence. This is because systems of intelligence hold the business logic that allows them to orchestrate services that are both internal to a company and external to a company. This allows them to adapt to changes in user interaction — able to dynamically respond to natural language queries from consumers, for example — as well as to facilitate the working of stateful AI agents, able to manage complex tasks with asynchronous execution.

Systems of intelligence to orchestrate data and business logic

Within financial institutions, there will be different use cases for probabilistic GenAI than for deterministic, machine-learning AI. The latter will be applied, for example, in any use case that needs to be explainable, such as a credit decision, whereas the former are likely to be used in providing assistance to internal and external users, such as “co-pilots” to help explain terms, navigate options and execute instructions, based on fine-tuned models to avoid hallucinations.

In effect, then, what is likely to emerge is a tapestry of models, based on different contexts and datasets, with seamless handovers between them. As an example, a concierge GPT may understand what a customer would like discuss, pass to another GPT that can discuss options for say an unsecured loan and which could complete an application process, but that would pass off to a ML algorithm to execute the loan.

If machine-learning models can get financial institutions to 100% straight-though processing, GenAI models can get them to 100% self-assisted transactions.

For all of this to happen requires more than just AI. Systems of intelligence will be needed to provide the orchestration between different systems and data, and to provide the business logic to make all of this seamless.

The optionality of systems of intelligence

Many financial institutions today feel overwhelmed. Their Linkedin feeds trumpet the promise of GenAI, but the reality on the ground is probably a handful of prototypes, an internal GPT portal, and massive backlog of use cases to triage and investigate.

The truth is that deploying GenAI productively is hard. It requires giving access to data to third-party tools (introducing procurement and compliance hurdles), it requires understanding which providers can actually help and for which use cases (when productivity savings are difficult to calculate and when it’s hard to see tangibly what many solutions do) and it requires integration into a myriad of organisational processes (which takes a lot of time to coordinate and roll out).

A system of intelligence not only allows for GenAI to rolled out more quickly, but it also buys a lot of optionality.

Orchestrating between multiple datasets and with a lot of inherent business logic, systems of intelligence provide a single operating system to automate multiple workflows, speeding up adoption, but also taking the pressure off organizations to prioritise use cases — since they can address use cases incrementally, leveraging the same initial investment.

As such, where investing in AI point solutions will likely improve productivity, system of intelligence allow for the progressive reimaging of organization structures and open up the possibilities for new business models.

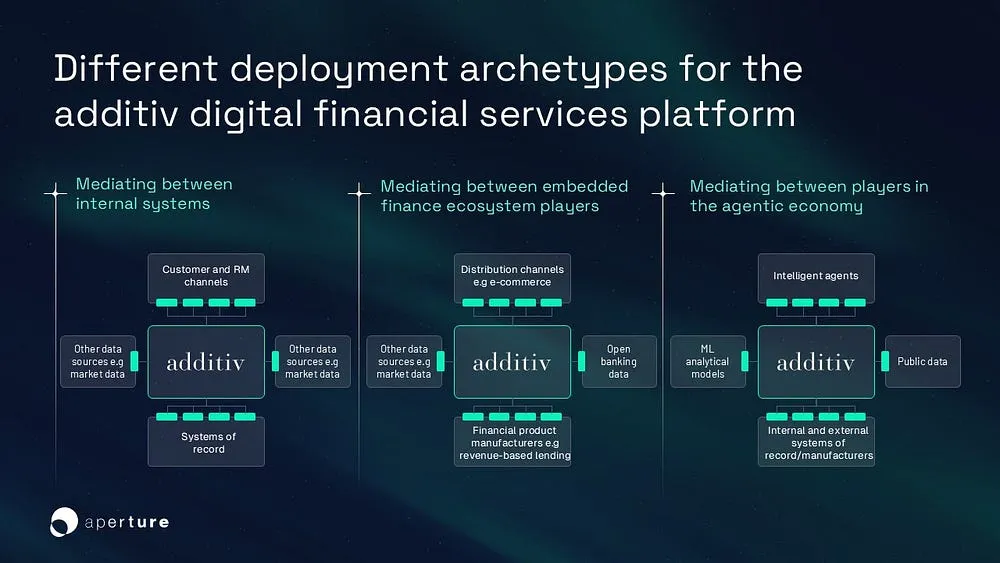

additiv — a case in point

additiv illustrates neatly the optionality of a system of intelligence and how it allows organisations to adapt to changing technology and market needs. additiv was designed to be a middleware layer sitting between systems of record and systems of interaction. Originally, it was used by private banks and wealth managers to provide seamless and rich interaction across multiple channels, whether self-service or advisor-led. The company then realised that the same architecture set it up perfectly for embedded finance, substituting multiple internal user agents with multiple external distribution channels, and substituting multiple internal systems of record for multiple external (or internal) product manufacturers’ systems of records.

Now, additiv and its customers have now realised, its headless platform, with the business logic to orchestrate a dynamic set of services, is also ideally suited to leveraging GenAI to automate processes.

To illustrate how well the additiv platform does this, consider how it is using AI agents in insurance use cases. In one, a user with a single prompt can ask if the damage to their possession is covered by their insurance policy and, if so, ask for an insurance claim to be submitted. The platform then handles the various steps, detecting what the object is, verifying that the damage is genuine, before reading the insurance policy, understanding what additional information is needed (e.g. a screenshot of the replacement item to establish the claim value), writing the claim and then submitting the claim. In short, one user request leads to AI calling multiple internal and external systems, before completing the end to end task.

Why adoption of systems of intelligence has been slow

Given the essential role of systems of intelligence to scaling financial institutions, to delivering rich customer experience, to facilitating embedded finance, and now to capitalising on the promise of GenAI, why haven’t we seen faster adoption?

Firstly, because platforms take time to mature. Since they operate as part of an ecosystem, platforms typically take a long time to build — or more precisely a long time for the ecosystem to coalesce — and, especially for two-sided and multi-sided platforms, the value grows as the ecosystem grows. Platforms like additiv have been building and deepening their value-add for years.

Second, while traditional financial services companies have been losing market share — and leaking the most profitable services first — market share erosion has been fairly gradual. Further, during the fintech winter, incumbents saw many of their fintech competitors go out of business or slow their rate of customer acquisition as VC funding dried up.

Thirdly, with rising net interest margins, bank profitability over the last 3 years has been as its highest for 20 years, reducing the need to seek efficiencies.

Lastly, we had a global pandemic. During that period, financial institutions diverted enormous resources to digital channels, to ensure that clients were able to self-service in the absence of physical interaction.

All in all, there was a lack of pressure to invest in orchestration systems, which is now changing.

Competition is intensifying…

There is no doubt that competition from digital-native players is hotting up. Many, such as Revolut, have hit escape velocity and are materially eating into the market share of incumbent providers.

…but GenAI is the biggest catalyst for change

As we wrote at the start, far from undermining the case for systems of intelligence, GenAI strengthens it.

In a classic case of what Union Street Ventures calls the app-infrastructure cycle, we have all seen the power of ChatGPT and Claude to revolutionize the way we interact with public information and the productivity savings that ensue. What we need now is the infrastructure to do this for complicated use cases in complex, regulated organisations.

This infrastructure is systems of intelligence and their day has come.

*********************************************

Note: Aperture has investments in additiv and Tuum, as well as several of the players in the “system of intelligence” graphic

Subscribe to our newsletter

Join our newsletter to stay up to date on features and releases.