Enterprise SaaS is not dead

TL; DR

There is no question that the software-as-a-service model is under pressure as GenAI lowers the cost of creating software, reducing pricing power and opening the floodgates for substitutes. But to suggest that SaaS is dead ignores the many prognoses of technology deaths that never came to prevail (e.g. the mainframe is dead). Software is sticky, and not all SaaS is created equal. Our view is that a lot of point solutions will gradually disappear, displaced by AI-first substitutes, custom-built solutions or subsumed within larger platforms like Microsoft Office or Google Workspace. However, we predict that, provided they invest in AI capabilities, the future looks much brighter for enterprise SaaS solutions that incorporate important systems of record (like Salesforce for CRM or Tuum for core banking) as well as vertical SaaS solutions, which we expect to become even more specialised. Moreover, we continue to believe we’ll see a surge in intelligent middleware that consolidates enterprise data and provides the necessary context for LLMs to work effectively.

The SaaS challenge

SaaS is under pressure for three main reasons:

- Commoditization of software functionality: GenAI is making it easier and cheaper to write software. This makes SaaS applications vulnerable in a number of ways:

- the generic tools like ChatGPT and Claude can already do a lot of what many SaaS applications do, such as data analysis, reducing the value of these applications;

- with falling costs, barriers to entry are falling and we are seeing a Cambrian explosion of AI-first new entrants, building specialist applications on top of LLM models, providing cheaper and better alternatives to SaaS applications; and,

- falling costs and complexity also allow enterprises to build custom software, exactly suited to their use cases and fine-tuned on their data, replacing horizontal applications.

2. Shift to usage-based pricing: GenAI is driving a shift from static, per-seat SaaS subscriptions to dynamic, usage-based or pay-per-task models. Instead of licensing software, users interact with AI models to perform tasks on demand charged by tokens or API calls, which breaks both the recurring revenue model on which SaaS vendors rely as well as reduces vendor lock-in since the natural language interface becomes the value layer, not the app.

3. Platform consolidation: the largest technology players like Microsoft (Copilot), Google (Workspace AI) are embedding GenAI into everyday productivity platforms. This creates a winner-take-most dynamic, where users default to built-in AI rather than paying for specialized SaaS tools. Essentially, the tool sprawl of the last two decades will gradually go into reverse as enterprises consolidate around broader platforms.

What kinds of SaaS applications are most at risk

For us, the litmus test of whether a SaaS application has longevity rests on whether it sits at a control point in the value chain — and these control points are changing.

As the user interface moves from apps to natural language prompts, a lot of systems of interaction will lose their point of control. Systems like customer support portals, application tracking systems or internal knowledge bases that rely on the manual introduction of information, manual triaging of information or manual responses will give way to AI-native tools, like Jaid and Supervised, that allow for much greater user self-service, where users interact with agents to answer their queries.

Similarly, many applications will lose their control as their functionality get replaced by AI. For example, Business Intelligence solutions rely on pre-built dashboards and structured query interfaces. But as users — or agents — query databases directly using natural language, the need for dedicated BI tools diminishes.

Others will lose their control point because they lack domain-specific knowledge and workflows. For example, where robotic process orchestration requires structured data and works by mimicking human actions (making it susceptive to UI or format changes), GenAI agents work in context-rich environments, such as additiv’s orchestration platform, and can route workflows adaptively.

Enterprise systems of record are defensible, but risk value leakage

Major enterprise systems of record — CRMs, ERPs, PMSs, CBSs, etc — have significant intrinsic defensibility. This arises from two principal areas. The first is that they do much more than customer interaction. In a much quoted interview, Satya Nadella said SaaS applications are just CRUD databases and likely to “collapse” in the agentic era. While, as acknowledged above, this may be true for many consumer apps and simple enterprise applications, for mission-critical applications, like core banking or fund operating systems, the vast majority of their workload is not handling user interactions, but handling everything that comes downstream of the interaction. Secondly, enterprise systems of record have a control point over critical information, which is not easily consumable by LLMs or agents. Record-keeping data is neither physically (as in indexing) nor logically (as in the way it organised) suitable for use by LLMs and needs significant reorganisation and enrichment.

The imperative, therefore, for the providers of enterprise systems of record is to invest in the systems of intelligence that will simultaneously allow them to retain control over their data and extend their relevance and importance by helping their users to unlock the value of GenAI. They need both to react quickly and invest early to avoid being pushed down the value stack by emerging systems of intelligence that can consolidate and orchestrate “intelligence” across multiple systems of record.

As explained in our last blog, on “digital era systems revisited”, we believe that we will see the emergence of “systems of intelligence” that are not proprietary to a single enterprise application. Essentially, this emerging infrastructure layer organises enterprise data and provides the logic and context for agents to resolve complex user queries and complex use cases within enterprise IT landscapes that normally comprise a complicated web of applications, processes and heterogenous datasets.

We predict that within the GenAI hype cycle we are entering the period where enterprises grow frustrated that their GenAI investments are failing to translate into material productivity improvements. The challenge is that, unlike implementing a discrete SaaS application, delivering meaningful productivity improvements rests on changing processes and ways of working quite broadly across companies. This, in turn, involves significant coordination, which, in IT terms, means consolidating multiple datasets and orchestrating multiple processes. This requires new infrastructure which sits between enterprise systems of record and existing and emerging points of customer interface.

We remain bullish on vertical SaaS

In contrast to standalone, albeit broad, enterprise systems of record, Vertical SaaS applications handle the end-to-end needs of their enterprise customers, making them both defensible and well-placed to capture the value shift that comes with GenAI adoption.

Vertical SaaS applications are defensible for the same reasons that critical systems of record are defensible. First, they hold the information that their enterprise users rely on to run their businesses. Second, they do much more than managing customer interactions, they support their users to manage the entire customer lifecycle.

However, they are better placed than enterprise systems of record for three keys reasons:

They control an already consolidated dataset

This puts them in the position where it is very difficult for an AI-first application or system of intelligence to disintermediate a vertical SaaS application from its users. The role of the system of intelligence is to consolidate and enrich enterprise data, but a VSaaS platform does already since it provides reporting capabilities to end users. An AI application needs to access the VSaaS data , which requires the VSaaS platform to acquiesce (or not). Even if they end up partnering with AI applications, they do so from a position of strength, able to capture the lion’s share of the value.

They are hedged against a drop in the cost of developing software.

First of all, like any software company, not just new entrants, the VSaaS platforms can capitalise on falling development costs to extend the capabilities of the platform to increase value-add and avoid price erosion. In fact, we predict that we’ll see a lot of new entrant activity in VSaaS since low development costs will enable providers to profitably serve smaller verticals and because embedded AI solutions will realise that, to compete effectively, they need also to control the system of record.

Secondly, and more importantly, because they are also in the distribution flow — that is, unlike standalone record-keeping systems, they are also systems of interaction — they are in a position to pursue indirect monetization, especially through embedded finance. Many of the most successful platforms like Shopify and Toast already generate the bulk of their revenues through embedded finance, but this will become more common for other VSaaS platforms, which typically only monetize payments today and will move to embed credit and insurance.

AI makes their business model better and more scalable.

Embedding more AI into solutions allows their users to save time and do more with the application, which underpins the utility and stickiness of the application. Potentially, to the extent to which a VSaaS provider can frame increased customer investment in new tools as a direct substitute to hiring new people, they may be able to tap into HR budgets as well as software budgets. In addition, for the users, opening up a natural language interface will create highly customised experiences at scale.

The same is true of internal users. This is especially interesting to VSaaS providers who layer on some form of business processing to their solution. Think about services like KYCing customers or sending out statements, which were historically human-centric and difficult scale. These can increasingly be automated now using LLMs and agents, which will allow these types of services to scale like software, and allow these VSaaS businesses to grow quicker with better margins.

We’ll illustrate how some of these trends are already playing out with reference to some of our clients.

Services-as-software

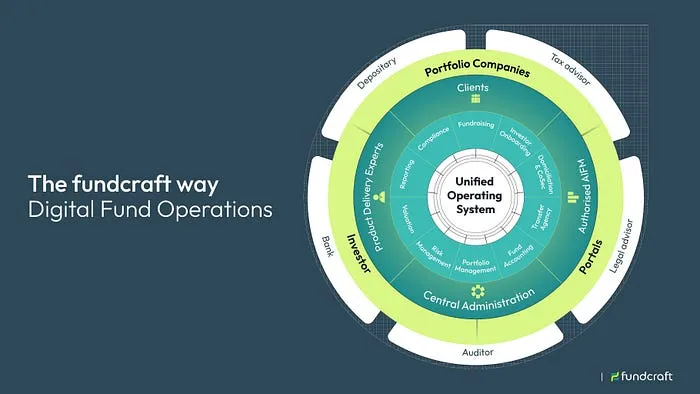

fundcraft is an example of vertical SaaS business whose value proposition combines technology and operations and which is investing in AI to make these operations much more scalable.

fundcraft provides end-to-end fund operations to alternative asset managers — everything from investor onboarding to regulatory compliance. Its competitive edge lies in extent to which it has consolidated fund data and automated processes, giving better accuracy, empowering greater self-service, and reducing costs vis-à-vis incumbent fund administrators.

Now, fundcraft is capitalizing on GenAI to go further. For example, fundcraft now fine-tunes models to produce board minutes and uses agents to manage multi-step processes like capital call execution. As a result, fundcraft operates increasingly programmatically, breaking the historically linear relationship between customer numbers and employee numbers, and unlocking a new level of scalability.

This services-as-software opportunity is likely to crystallise for new vertical SaaS entrants like fundcraft vs incumbent providers for two reasons.

The first is that they do not have any business model conflict in automating processes end-to-end. In the case of fundcraft, they do not charge the task- or people-based fees of a traditional services business, nor do they charge a user-based SaaS fee like a classic software company. Instead they charge a fee based on deployed capital, giving every incentive to automate as much as possible.

The second is that VSaaS solutions consolidate mutiple datasets. In the case of fundcraft, all of the accounting, fund management and compliance data is in one place. This is what makes it possible to bundle more capabilities — LP reporting, valuations, payments etc — but also gives it control over the data needed to train and fine-tune models that will automate processes and ensures that it acts as the nexus for other operators in the fund value chain, such as auditors and depository banks. In the agentic era, coordinating activities across fragmented actors and workflows will be the biggest source of value creation.

Indirect monetization, custom experiences without the custom code

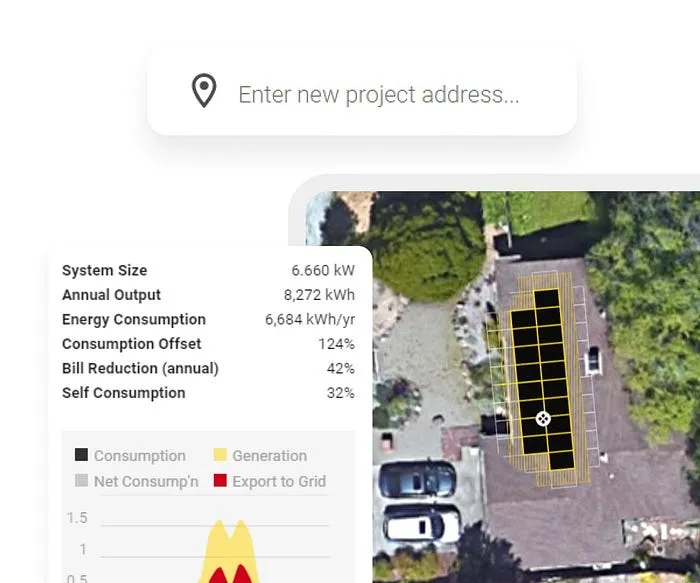

OpenSolar provides a comprehensive VSaaS application for solar contractors, the operating system on which they run their businesses, simplifying reporting, material ordering, invoicing, cash collection and much more. The difference from other applications on the market is that it is free to use. This represents a compelling proposition for all contractors: those running their businesses on a patchwork of tools (excel, email etc) can move for free to an integrated application, while those already using purpose-built software can save themselves the cost an expensive monthly SaaS subscription. As a result, the application is rapidly taking market share — for example, in the UK it reached 50% share just 18 months after launch.

The monetization is all indirect. OpenSolar takes a small slice of the GMV going through the platform by, for instance, taking a small fee on the hardware ordered and a taking a few basis points on payments handled within the app. In effect, it does what the best platforms do, maximizes network effects first and monetizes later.

The OpenSolar model might be the blueprint for VSaaS new entrants. First, it is almost impossible for incumbents to copy the model, who face the innovators dilemma of having to cannibalise their existing model on which evrything is optimised. Second, as already mentioned, it protects against a general deflation in SaaS pricing. Lastly, in VSaaS models where, like OpenSolar, there is both demand and supply aggregation and strong network effects, the indirect prize is likely many orders of magnitude bigger.

OpenSolar is also capitalising on GenAI. In its case, it is opening up opportunity to enterprise users to converse with the system in the way they might with ChatGPT. With v3.0 of the app, out next month, users can generate the information they want or instruct the system to do what they need, giving them a simple natural language interface into their business operation. It is, in effect, a wholly customised experience, but without any of the custom code or custom services that historically made this either prohibitively expensive or prohibitively difficult to scale.

In summary, not all SaaS is created equal

It is axiomatic and even trite to say that all software companies should be investing in AI. However, for some, investments will be focused on vulnerabilities now exposed by GenAI, while for others the investments will extend their competitive advantage. Our view is that the dividing line between the two is control over key data and workflows. Critical systems of record and Vertical SaaS solutions are well-positioned to capitalise on this inflection point, while systems of interaction are not.

Subscribe to our newsletter

Join our newsletter to stay up to date on features and releases.