Fintech All the Way Down

In his report on European competitiveness, Mario Draghi proclaimed that “Europe is faced with an unprecedented need to raise investment at both massive scale and rapid speed.”

By Draghi’s estimates, Europe needs to invest an additional €750–800 billion annually to restore sustainable growth, boost productivity, and remain internationally competitive, with investment needed chiefly in energy, transport, digital, telecom and defence.

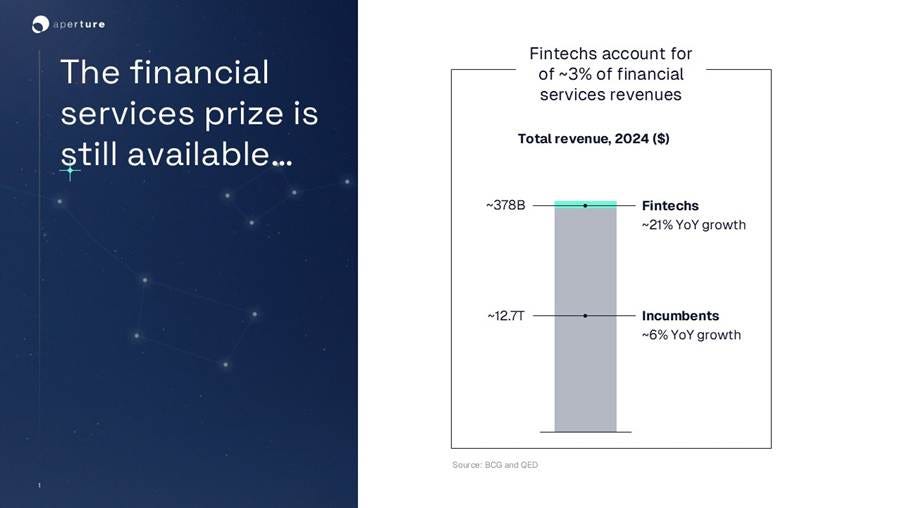

Against this context of urgent infrastructure investment, together with the emergence of generative AI which promises to codify away millions of jobs as well as codify software building itself, we hear about the imminent demise of so many things. Software as a service is dead (replaced by GenAI), venture capital is dead (replaced by debt and government financing of hard assets), Europe is dead (surpassed by the US and China). It follows, therefore, that VC investment in European fintech software must be profoundly dead, dead³.

However, we would argue that there has never been a better time to invest in European fintech. Why? Firstly, because we are entering into a new wave of fintech, an agentic and programmable phase, that is poised to democratize complex and expensive to serve markets. Desirable in itself, this democratization will also play a significant role in improving financial intermediation and getting Europeans’ savings into productive assets (as Draghi entreats us to do). Secondly, because new fintech infrastructure is essential to move from the installation to deployment of generative AI. And, thirdly, because with software subscription revenues under pressure (as GenAI lowers the cost of software development) and inference costs running ahead of AI app subscription pricing, embedded finance will become a more important lever for monetizing tech businesses.

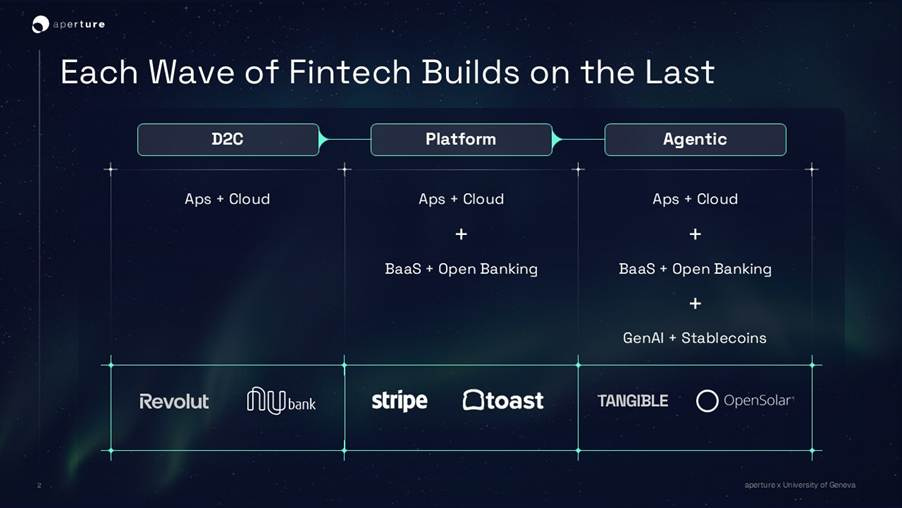

Every wave of fintech builds on the last

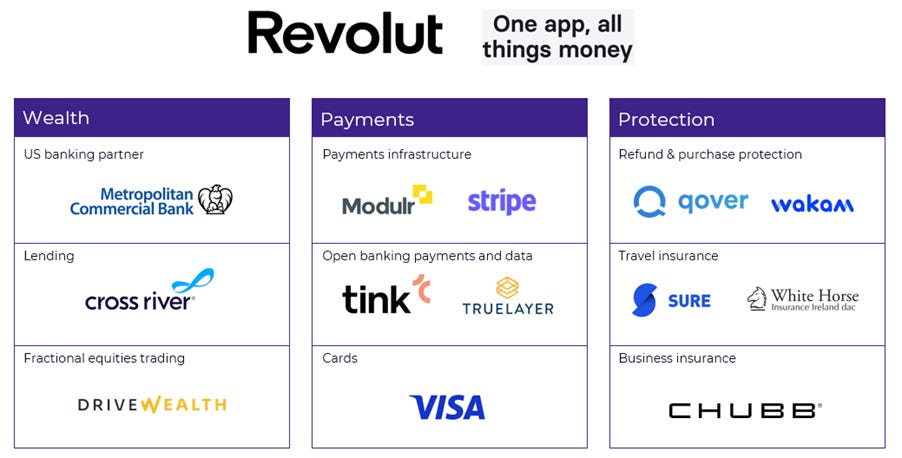

The last wave of fintech created many industry giants. To give just a few examples, consider Revolut (now the largest European bank by customer numbers), Stripe (which processes 1.5% of global GDP), Circle (a bumper IPO in 2025 with over $60 billion of stablecoins in circulation), Plaid (empowering over 2,500 fintech businesses) and Toast (a VSaaS platform for restaurants which makes a cool $4.5 billion from payments).

As well as massively successful in their own right, these companies embody major infrastructure upgrades in the fintech landscape that will underpin future waves of fintech innovation.

Mobile banking apps, running on cloud computing infrastructure, have transformed customer engagement and enabled the most successful players like Revolut and Nubank to become aggregators of their own and third-party services.

Open banking facilitates the exchange of information that has fostered innovation as well as helped to open up financial services distribution to non-bank channels and, in time, to agents.

Stripe is an archetypal example of the BaaS infrastructure that now exists to convert regulated financial products into APIs that can be plugged into any distribution channel (like Toast).

And stablecoins are a breakout use case of the blockchain infrastructure that has been built out since Bitcoin white paper in 2008 that renders money both programmable and capable of being moved 24/7 without intermediaries.

The current wave of fintech will usher in massive democratization

Building on this infrastructure and combining with GenAI will enable entrepreneurs to tackle areas of financial services provision that have remained stubbornly resistant to change and digital disruption.

Take wealth management, for example. The costs of acquiring time- and attention-poor HNWs have historically run to tens of thousands of dollars. On top of this, there are the high costs of onboarding and ongoing compliance checks and even higher costs to serve (providing personalized portfolios, personalized customer service, personalized reporting, etc). Unit economics have stayed high despite changes in delivery channels and this has placed a ceiling on the size of the market (to the detriment of millions of mass affluent and retail clients who would benefit from professional wealth management services).

This is now changing. GenAI is different from the automation tools that preceded it. It can do much more than just perform repetitive tasks faster. GenAI can explain complex financial decisions in plain language, learn from past interactions, generate personalized content, and adapt in real-time. As such, it can handle onboarding, portfolio construction, regulatory checks, and customer communications — all at scale, all personalized, and all at much lower cost.

Furthermore, when you layer GenAI on top of other fintech infrastructure, you start to see the compounding effect. Embedding wealth management into existing applications, like say a payroll app, provides access, data and customer context. GenAI can then handle the onboarding and create personalized portfolios. Smart contracts could then auto-rebalance the portfolio according to pre-agreed rules. The result: lower CAC, lower cost to serve, higher customer satisfaction and a much larger addressable market.

This transformation won’t be limited to wealth management.

Commercial insurance, treasury, private market investing are all areas in which we have made recent investments. The reason is that, like wealth management, they have all historically suffered from the same problems of high complexity and high cost to serve that are now being solved.

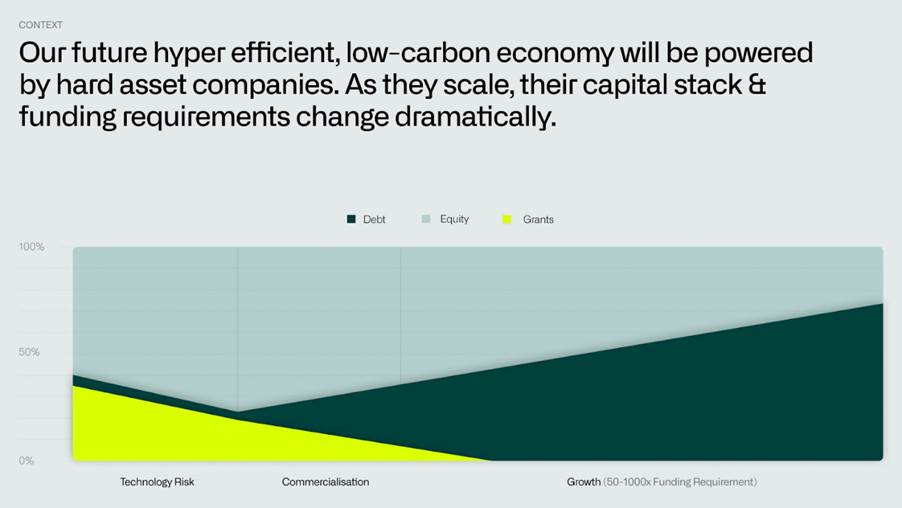

Consider this also in the context of Mario Draghi’s call to action. The annual debt financing gap for European (ex-UK) SMEs runs at about EUR40billion because high onboarding, credit scoring and servicing costs make it uneconomic to lend, especially where there are no fixed assets to collateralize. Even where there are hard assets to collateralize, the complexity and opaqueness of products like asset-backed financing, as well as the lack of understanding of specialist new asset classes (what’s the residual value of a hydrogen electrolyzer?) still make it hard to get lending flowing to the right places.

But, again, entrepreneurs are leveraging new technologies to address this. Vertical SaaS companies like Ferovinum (for wine makers) get closer to the data and to the assets, allowing them to underwrite risk more cheaply. Product innovation is happening, like Bourn’s smart business overdraft, which leverages data from SMEs’ accounting systems to secure overdrafts against accounts receivable, dramatically lowering fees. And new platforms are emerging, such as Tangible, which makes the bridge between private capital funds and hard asset startups, helping ready the startups, arrange and negotiate the term sheets, and provide real-time reporting.

In private market investing, digital infrastructure platforms like fundcraft are helping to empower new innovative asset managers like Stableton, which brings index-based investing to private stocks, lowering the fees and changing the liquidity profile of private equity investing.

But advances in fintech won’t just lead to advances in financial services

To paraphrase Robert Solow, you can see GenAI everywhere but in the productivity statistics.

A recent, oft-quoted MIT study, suggested that 95% of GenAI projects fail to deliver enterprise value. This is perfectly normal. In what USV calls the app-infrastructure cycle, we first get the breakout app (in this case, ChatGPT) and then we need to build out of the infrastructure to enable this experience to become pervasive across every use case, especially for enterprises.

What fintech infrastructure is needed to move GenAI into its deployment phase? Here are a couple of examples:

1. The infrastructure for agentic payments and billing. Our existing payment and billing infrastructure was built for humans. It’s calibrated to identify humans and look for human-perpetrated fraud (already an issue pre-agents). It’s engineered for human speed, not for agents that can make hundreds of decisions instantly. And it’s optimised for in-checkout payments and subscription billing, not for usage-based models based on variable compute. This has to change – and is changing. Paygentic illustrates how fintech entrepreneurs are already moving to solve these problems. Paygentic allows for monetization of any billable metric – even for granular micro-transactions - enabling subscriptions but also usage-based, outcome-based, and hybrid models.

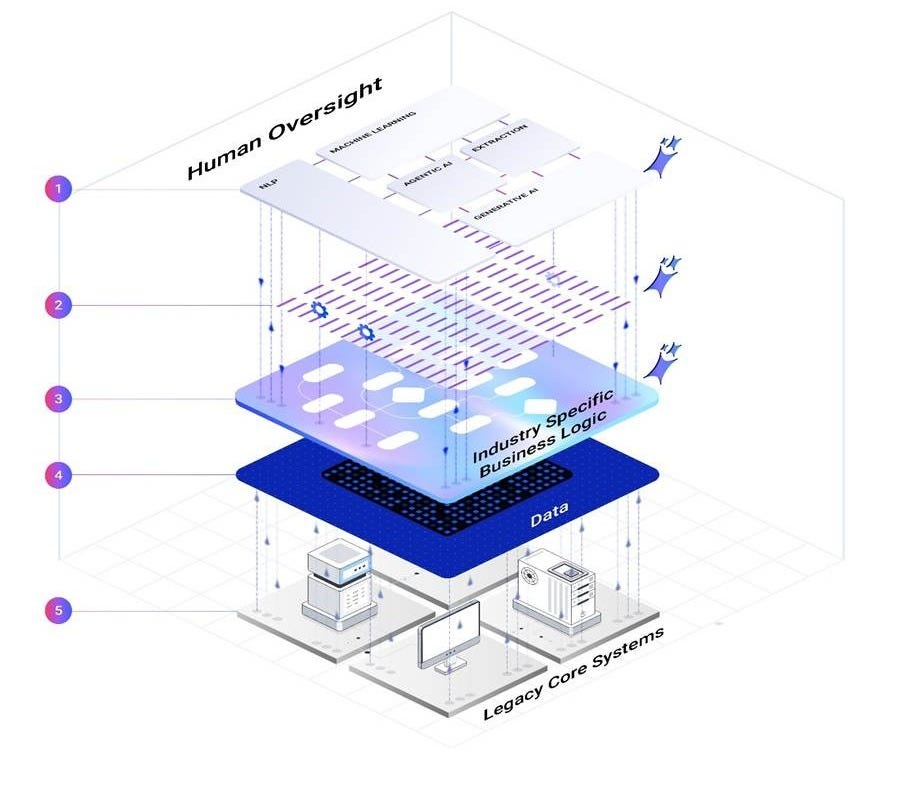

2. Getting LLM models ready for enterprise use cases. What would be ideal is if you just could plug an LLM into enterprise data and it worked like ChatGPT does. However, a number of obstacles have to be overcome before this can happen. First, it’s necessary to fine-tune the models for given use cases. Second, it’s necessary to aggregate data from multiple internal systems to give the right contextual information to the LLM. Third, it’s necessary to transform that internal data physically and logically so that an LLM can understand it. Moreover, if a company then wants to you use agents - that is, LLM models that can act on information (as opposed to just chat) - it then needs to make available domain-specific rules through APIs that define how things are done in its business and industry. This kind of orchestration across models and datasets is very complex for companies to do, but happily there are tech firms providing platforms to make this easy, with additiv being the pre-eminent example for fintech.

Fintech will become even more important as a monetization lever

Last week, one of our portfolio companies, OpenSolar, announced $20m in fresh funding in a round led by Google. OpenSolar (OS) provides the #1 vertical SaaS application to solar contractors. The company is growing incredibly fast, buoyed not just by a surge in energy demand globally but by the fact that, unlike the competition, its app is free. Rather than charge a SaaS fee, OS has an indirect revenue model. It makes a small margin on financial services originated through the app.

OpenSolar is a useful case study.

Firstly, it’s a fintech company (in our definition, at least) that meets many of the Draghi tests in that 1) its data is being used to lower the cost of lending to SMEs (solar contractors) and hard asset companies (solar panel and battery producers) and 2) in providing free software to the energy sector, it is directly helping to accelerate the rollout of clean energy.

But, secondly, it’s an example of what we believe will be a growing trend towards providing software for free and monetizing through financial services. This distribution strategy makes increasing sense both for defensive reasons (to protect against falling subscription revenues) but also for offensive reasons (since maximizing user numbers maximizes network effects and also provides the data to train models, both deterministic (like credit scoring) and probabilistic (like AI agents).

In addition, it’s quite likely that AI-native companies will explore embedded finance as a way of aligning their revenues better with customer outcomes. At the moment, AI-native firms have the MoviePass problem of having fixed revenues alongside uncapped marginal costs. And every time they increase their subscription fees, churn picks up. We expect this conundrum to be solved, first, by metered pricing and then by borrowing from the VSaaS playbook by adding wallets, embedded payments, embedded credit, embedded insurance and more…

Fintech is a horizontal, not a vertical, market

The title of this blog is a reference to Packy McCormick’s excellent and prescient article “APIs All the Way Down.” In it, Packy talks about how APIs abstract away complexity to make everything plug-and-play. This is true of finance, and Packy uses the example of Stripe to show how finance becomes a set of composable, monetizable services at the disposable of any company with distribution power. But with the next wave of fintech, we’re about to go further. We won’t just abstract away complexity, we’ll simplify it. We’ll reduce the complexity and cost of compliance and customer service and we’ll remove intermediaries to speed up processing and settlement. This will have first order effects on the accessibility and availability of financial services. But it will also have second order effects in helping fund and make possible the infrastructure build out that will make Europe great again.

Subscribe to our newsletter

Join our newsletter to stay up to date on features and releases.