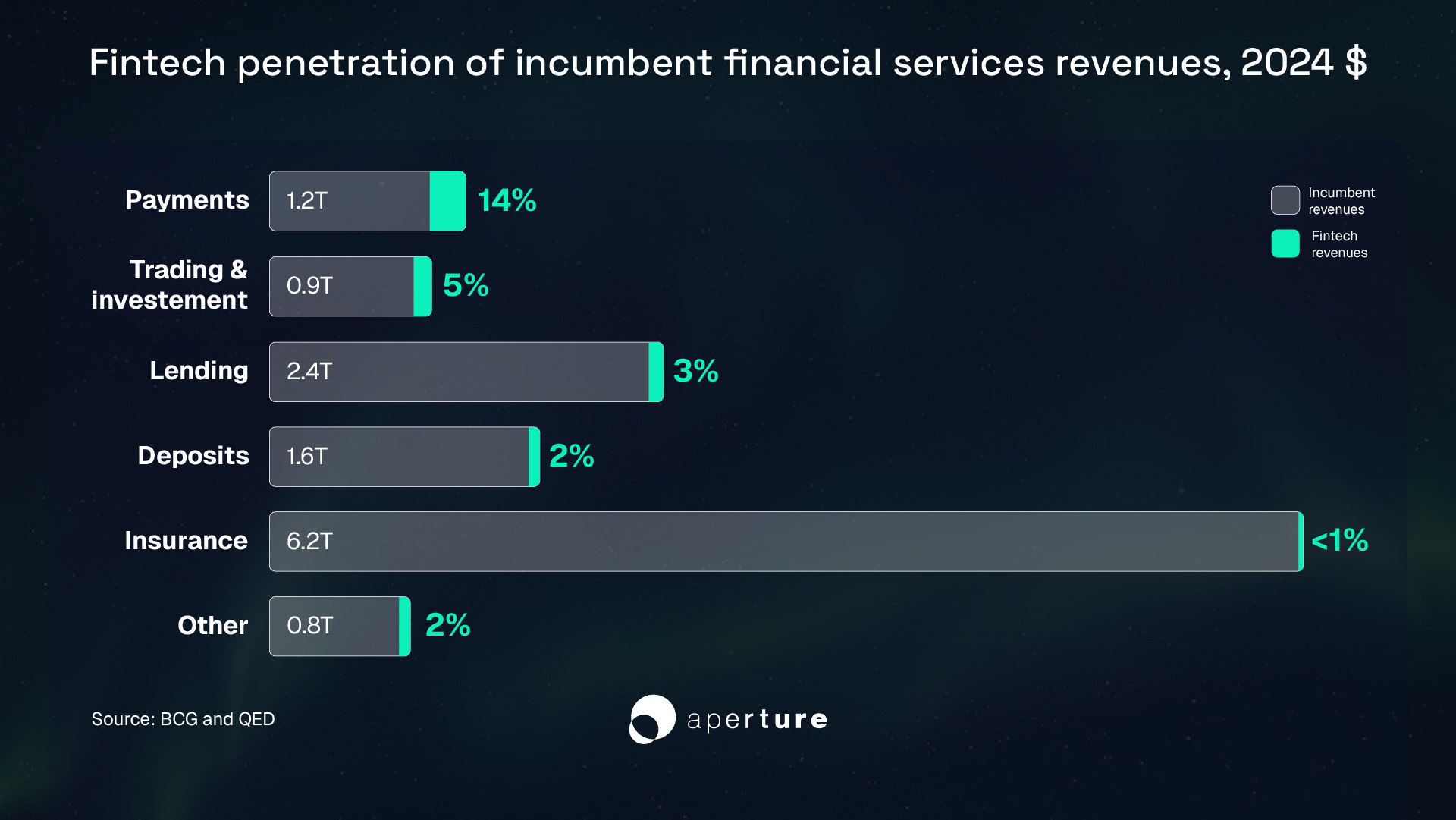

From Rails to Code: The Transformation of Payments

Payments is the area where incumbents have seen the most disruption from “fintech” players and many consider the payments landscape to be already quite settled. However, AI and crypto are about to unleash another wave of innovation, removing intermediaries and human oversight, making possible payments of any amount and at any level of complexity with infinitely parameterizable pricing, transforming the economics of commerce.

From Legacy Rails to Digital Networks

Payments have long been the unassuming backbone of finance: high in volume, low in margin, and reliant on coordination and shared standards. Making payments work was never really about innovation—it was about synchronizing vast networks, ensuring security, and maintaining reliability. Money shouldn’t be sent twice or end up in the wrong account.

Because payment systems needed to operate at massive scale, and now globally, they evolved into infrastructure built for endurance rather than fast iteration. Banks and regulators treated payments as plumbing: necessary, but too systemic to tinker with. For decades, caution limited experimentation, preserved legacy systems, and kept incumbents dominant. Wanting to innovate in payments was like trying to lay a new railway track while the train was moving. Everyone knew the system was rusty, clunky, and in need of an upgrade, but the fact that it worked was enough to keep innovators at bay.

That is not to say nothing happened. In the 1980s, the rise of electronic payments marked the first wave of change, enabling larger volumes and giving individuals electronic means of payment through debit and credit cards. Banks embraced this change, creating the consortium-operated shared infrastructures that became Visa and MasterCard. Retailers combined payment and loyalty cards primarily to accelerate their cash conversion cycle—collecting funds faster while deferring payouts to suppliers—while American Express focused on serving cardholders directly, encouraging merchant adoption through incentives and building strong network effects in the process. In another segment, payroll management provides an early example of complex payments executed in bulk, typically requiring bespoke solutions and tailored oversight to ensure timely execution.

The real signs that radical innovation in payments was possible only began to appear in the 1990s, when the Internet became critical infrastructure and both individuals and businesses started exploring its potential.

First, there was the Internet migration itself. As the economy moved online, payments followed—but without a native protocol. The web had HTTP, email had SMTP, yet payments remained tied to banking networks and hard to embed in websites or mobile apps in a standardized way. This gap led to internet platform pioneers to monetise mostly through advertising at the same time as it invited private solutions to try to solve this problem of native payments.

PayPal was an early success story, offering users monetary incentives to open wallets and developing an anti-fraud framework that later inspired elements of Palantir’s founding. From 2008 onward, Apple’s iTunes and the App Store provided a secure payment service for app developers. Around the same time, the Bitcoin white paper proposed a protocol for transferring value online—a concept later scaled by companies like Adyen (founded in 2006) and Stripe (founded in 2010—and now the poster child of reinventing payments globally). Each of these solutions contributed to bridging the divide between online demand and older financial rails.

Second, consumer payments were gradually streamlined. The 2010s saw the rise of increasingly diverse payment cards, driven not only by neobanks but also by innovations in aesthetics, materials, security, and embedded financial features, turning them from functional tools into personalized lifestyle products. At the market level, regulators and authorities forced broad upgrades, particularly in Europe, giving users conveniences like open banking, the PSD2 directive, and instant payments within the SEPA system.

Third, China’s payment revolution, led by WeChat Pay, accelerated mobile payments almost overnight. In 2014, Tencent introduced its digital red envelope feature during Chinese New Year, and usage exploded from 16 million packets that year to 1 billion the next. By 2016, during the festival week, 516 million users sent 32 billion red envelopes, turning a cultural tradition into a powerful tool for onboarding bank‑linked wallets. This social‑driven growth helped WeChat Pay reach hundreds of millions of users, embedding mobile payments into daily life.

Finally, today, crypto and AI are reshaping payments once more, opening new possibilities for speed, security, and programmability, though widespread adoption of some applications remains in progress. Innovations such as smart contracts, real‑time fraud detection, and AI‑driven personalized payment experiences are beginning to demonstrate how these technologies could transform the way money moves and is managed.

Mapping the Payment Landscape

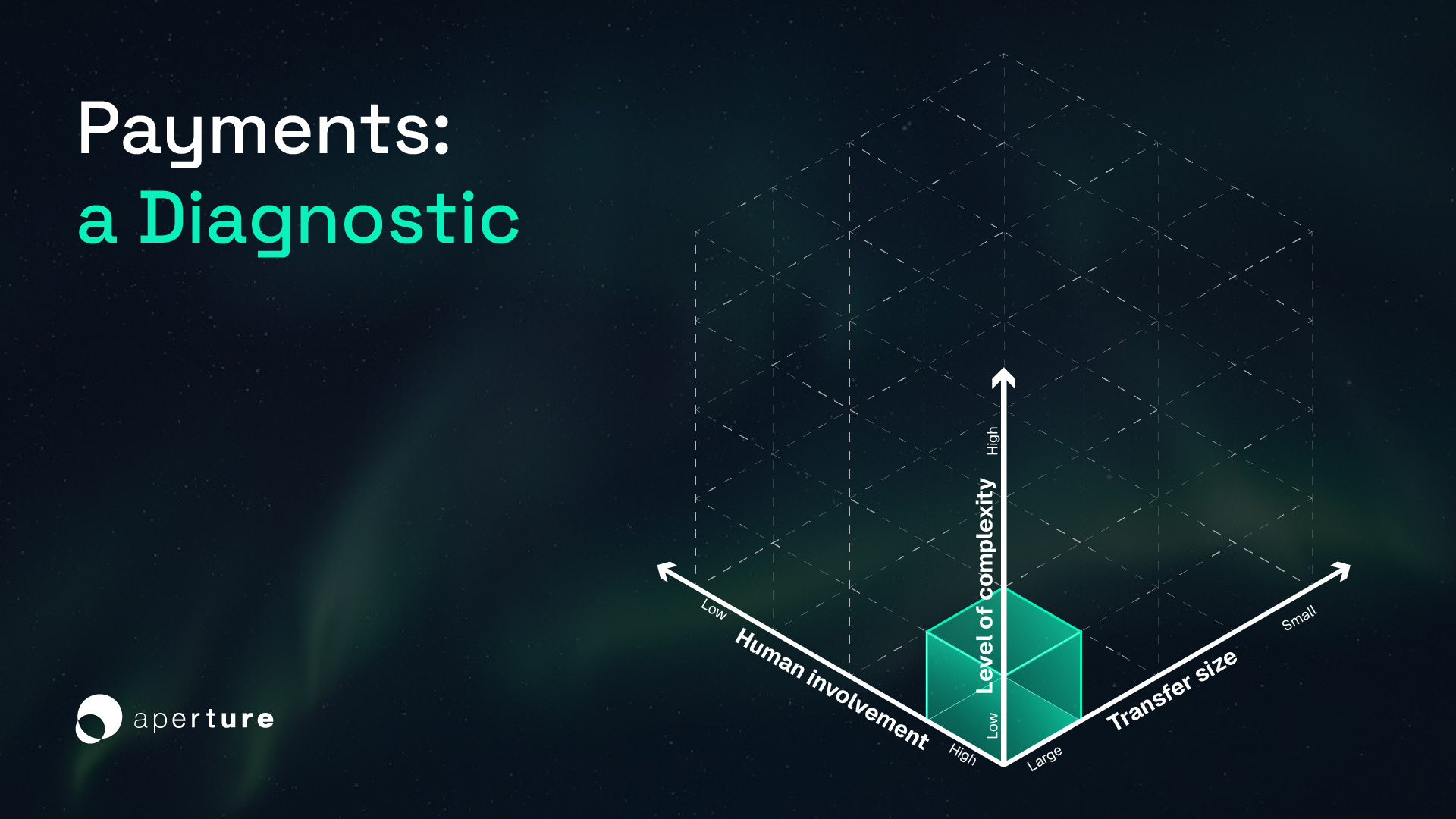

To understand how payments are evolving, it helps to visualize electronic payments along three dimensions: (i) the size of the transfer, (ii) the level of complexity, and (iii) the degree of human involvement. One axis runs from large to small amounts. Another runs from simple one-step transfers to those with many rules or parties or jurisdictions involved. The third runs from human control to autonomous systems.

For most of the digital era, only a narrow part of this space was active. Large, simple, human-supervised electronic payments dominated. They justified the cost of the rails and matched the cautious approach of banks and regulators. Other parts of the model stayed unused. Small electronic payments were too costly because fixed fees, fat margins for those who owned the pipes, and bad user experience made them hard to sustain. While small retail payments did take place, they often did so in cash and cheques rather than electronically. Complex electronic payments depended on manual checks, long chains of service providers, and reconciliation across different ledgers. Autonomy was effectively impossible, as each step required human sign-off.

This way of looking at the market shows the gaps clearly. The upper half of the model functioned but under strain: large electronic payments moved, yet settlement was slow and fees stayed high. The lower half barely functioned digitally. Systems built for high-value transfers could not handle low-value, high-frequency cases, and adding complex rules only raised costs and blocked innovation.

Tokenization shifts this picture. When rules, compliance, and settlement live in shared code, the cost of running a payment falls. Large transactions gain faster and cleaner settlement. Small electronic payments, which once failed due to fixed fees, become practical in many contexts. Complexity becomes manageable rather than a reason to block new ideas.

A third dimension is now emerging: software agents can send, receive, and coordinate payments within set limits. This reduces the need for humans to approve every step. Autonomy changes the economics of frequency and coordination, allowing far more electronic payments to move without friction and enabling conditional or multi-party flows.

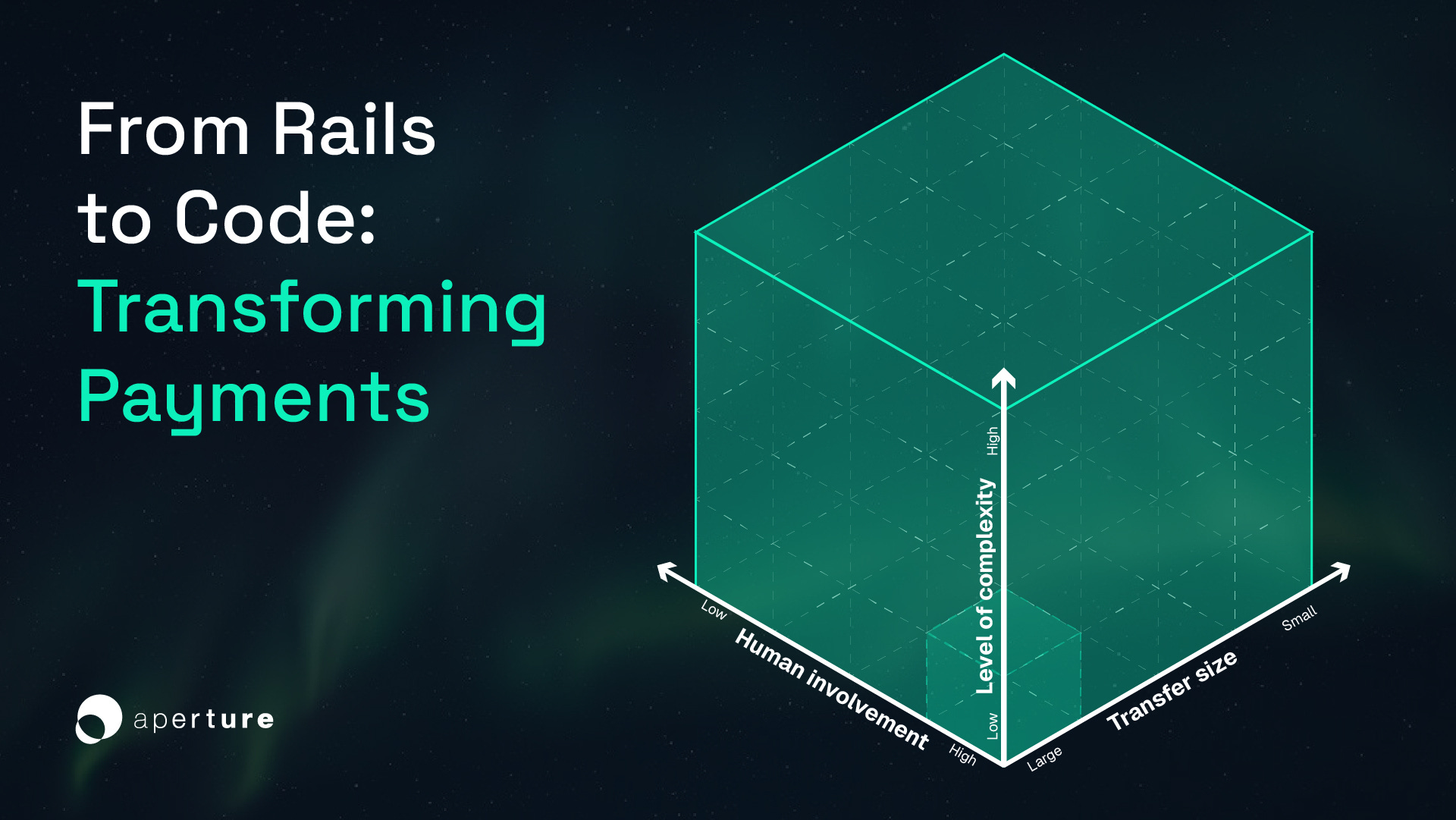

Once tokenization and agentic systems combine, previously dormant parts of the model begin to activate. Small and complex electronic payments can now exist, and large complex ones become less cumbersome. What began as a narrow space shaped by large, simple, manual electronic payments evolves into a broad, active field. Every point in the model can now support a viable payment flow, and electronic payments shift from a constrained subsystem into a programmable layer that can support many use cases across the digital economy.

High-Value Flows: Legacy Rails and Friction

Large payments—such as those between customers and suppliers in supply chains, or in financial transactions like an investment firm acquiring a company or distributing proceeds to shareholders—have always been cumbersome. Layers of KYC/AML checks and intermediaries—law firms, banks, settlement platforms, FX operators—phone confirmations, intraday and multi-day settlements, and high fees made the process slow and complex. But the hassle and cost were justified by the high stakes and sensitivity of moving large sums between demanding counterparties.

These payments exist, but the systems behind them are extremely fragmented, predominantly local, and ultimately inefficient. Settlement takes days, reconciliation is often manual, and fees remain high. The function is real, but the rails are strained. Large payments, while supported, demonstrate the limits of legacy infrastructure, highlighting the inefficiencies that innovators aim to address with tokenization and automation.

Micro-Moves: Small Payments Made Possible

By contrast, small payments, long uneconomic due to fixed costs, started to be addressed in the 2000s by Apple’s iTunes model. Steve Jobs introduced a key innovation: enabling users to buy music by the song rather than the album. This required skillful negotiation with music labels and leveraging Apple’s ecosystem control to overcome resistance.

Once the deal was secured, Apple faced another hurdle: enabling payments as small as $0.69 or $0.89 using payment cards without being overwhelmed by issuer fees. Apple solved this through a combination of innovation and leverage. The company accumulated credit until the total was high enough to pay fees in bulk settlements, effectively buffering the electronic payments system, which had previously made such small transactions infeasible.

This approach made micro-payments feasible, scalable, and profitable, transforming the economics of small-value digital transactions. Apple’s control over both content and payment flows unlocked new possibilities for small-scale digital commerce, demonstrating how thoughtful system design can overcome structural barriers to efficiency.

However, Apple abstracted away from the complexity and legacy of existing payment rails, rather than solving the underlying complexity. The same could be said for Stripe, which makes it easy for businesses to accept payment, effectively removing the need for them to deal with banks, credit cards, security, fraud, global currencies, and a lot of technical rules. But they haven’t fixed the rails and low value payments are still expensive.

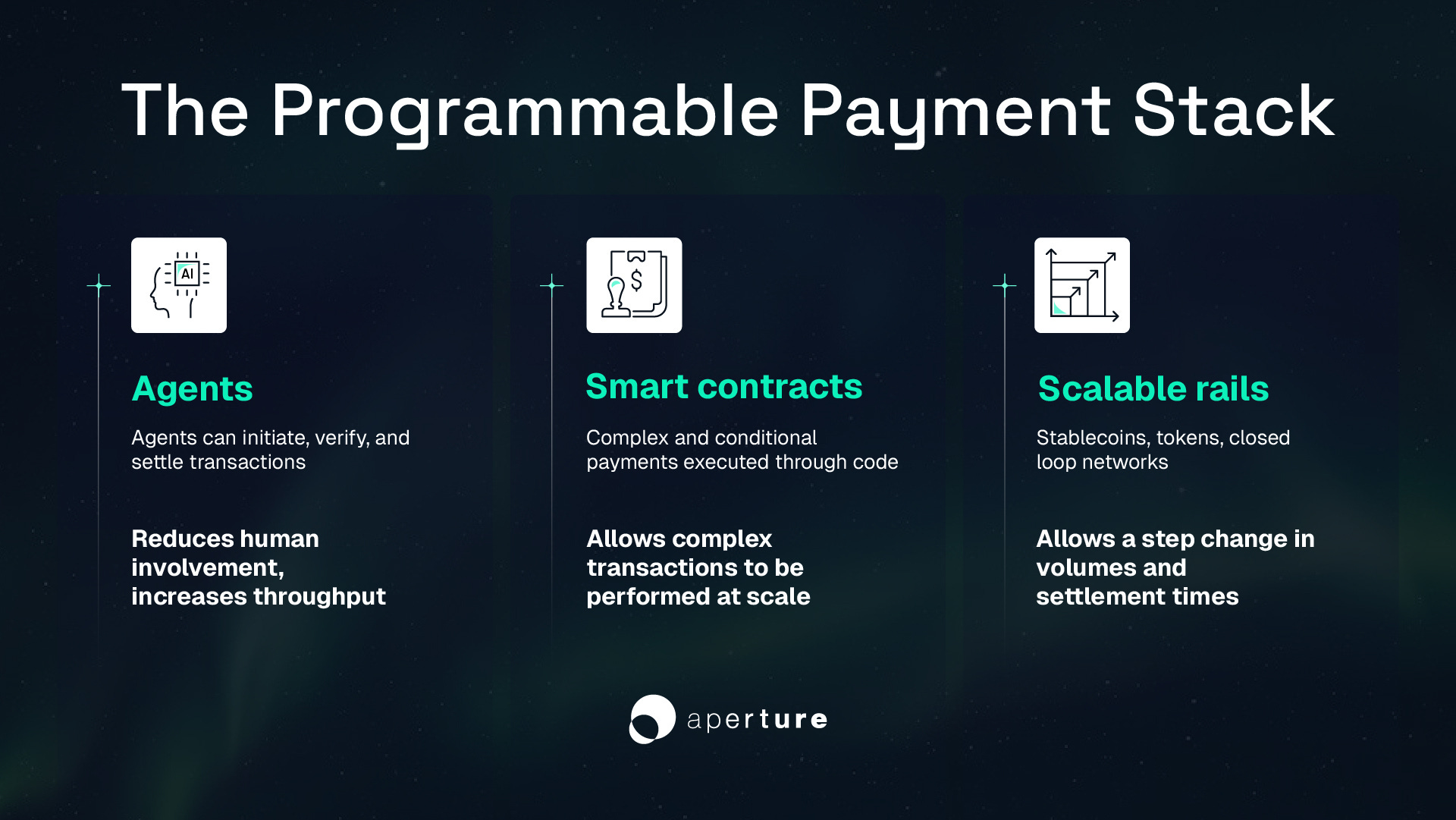

What comes next will be entrepreneurs fixing the rails. Removing intermediaries and batches using blockchain and other means to lower costs and improve throughput. Stablecoins for international payments. Tokens for P2P payments. Closed loop systems for agentic payments.

Structured and Smart: Tokenization and Smart Contracts

At the opposite end of the simple–complex spectrum are complex payments, such as those triggered for holders of structured products, laden with thresholds, covenants, multi-layered financing, and intermediary payments. Historically, complexity was a high barrier, reserving these transactions for multimillion-dollar deals involving deep-pocketed counterparties. They relied on a broad array of service providers—lawyers for drafting and reviewing documentation, accountants, custodians, bankers, compliance officers, and others.

This is beginning to change with tokenization. As analysts like Michael Green note, tokens can embed financial structuring directly into code, making complex payments more efficient and potentially cheaper—even for smaller amounts in pilot or experimental contexts. In an issue of his newsletter Yes, I Gave a Fig, Green simulates a tokenized bond portfolio that divides returns into senior and junior tokens, automatically allocating yield and risk via smart contracts. Processes that once required law firms, trustees, and intermediaries can now run as transparent logic on a blockchain. Generative AI further allows these structures to be explained simply to any interested user.

Thus tokenization transforms structured finance from a bespoke service into programmable infrastructure. Payments become as smooth and efficient as executing lines of code, regardless of complexity. Friction is reduced, minimum viable scale falls, and complex products—and their payment flows—become accessible to smaller investors, though widespread adoption is still emerging.

Autonomous: Delegating to Agents

Adding autonomy takes this further. Software agents can initiate, verify, and settle payments within defined limits. This removes the bottleneck of human oversight at each step while maintaining critical checks at the design and audit stages. Combined with scalable infrastructure, agentic layers can dramatically increase transaction volume. One person could oversee a million payments per day rather than a few thousand. With the addition of programmable money, markets for small, complex, or conditional payments become viable. Payments increasingly occur continuously and invisibly, embedded in processes rather than triggered manually.

Activating the Full Matrix

With these advances, all nine quadrants of the payment matrix become active. Whereas payments once had to be large or standardised to justify sophisticated electronic processing, they can now be operated digitally across any mix of size, complexity, and autonomy. This marks a broadening of the payment market. Payments can move in any amount, at any level of complexity, and without human involvement at any stage.

From a market perspective, this has two major implications. First, the number of transactions is likely to rise manifold. Second, businesses and individuals can now parameterise payments in more customised ways, no matter how niche.

This, in turn, will unleash a wave of product and value innovation. Offers can be tailored more precisely to local contexts, and previously underserved markets will become bright opportunities for entrepreneurs. In the past, only large, simple, human-supervised transactions were feasible. Now, even small, complex, agent-driven payments can occur efficiently.

This shift transforms payments from a constrained subsystem of finance into a programmable layer that underpins every digital interaction across the global economy.

Liberation of Pricing

The first major consequence of micro payments is the liberation of pricing. As the brake is lifted on the volume and value of transactions that can be processed, pricing itself can be dynamic. Traditional models—subscriptions, per-seat licences, or flat fees—will give way to usage-based, performance-linked, or hybrid approaches. In AI-driven contexts, this is becoming an urgent (and sometimes existential) need. AI companies have variable costs that scale with compute, data, or agent activity, whereas their revenues are based on subscription pricing, leaving them heavily exposed to losses, especially for heavy users. For them, it is imperative to align pricing with actual value consumed and delivered.

Companies such as Paygentic, in which Aperture recently invested, illustrate this trend, offering companies a payment and billing platform to monetise based on any measurable metric, including usage, outcomes, or micro-transactions. They show how billing can become continuous and automated, allowing revenue to track real consumption rather than predetermined cycles. Paygentic is an early and promising example of the infrastructure emerging to support dynamic pricing at scale.

Liberation of contractual payments

Even before programmable money, we have seen programmable payments. Trustap, an Aperture portfolio company, provides a programmable escrow service that sets the conditions under which P2P payments can be paid out. For instance, a seller of a concert ticket will be paid when the buyer of the concert ticket signs for the delivery through the mail (and this information is sent via API to Trustap.)

This level of programmability will go mainstream as these conditions are written into money itself through smart contracts. Payments will be executed automatically, triggered by usage events or outcomes, without requiring manual oversight. The cost per transaction falls, and businesses can implement finely tuned, usage-aligned pricing models that were previously impossible under legacy infrastructure.

Across industries, this opens new possibilities. Software, media, and even manufacturing can adopt flexible models that reward efficiency, align incentives with outcomes, and support granular microtransactions. Businesses can experiment with hybrid models—combining subscriptions, pay-per-use, and outcome-based fees—without being constrained by fixed billing systems or human supervision.

Ultimately, the liberation of pricing transforms the economics of commerce. Companies can capture and transfer value in real time, align revenues with actual consumption, and design business models around what customers truly use and value. Paygentic exemplifies how this can work in practice, but the principle extends broadly: programmable, agent-driven payments make pricing a fluid, continuous, and responsive element of modern business strategy.

Systemic Risk and Adaptive Regulation

As payments become code, regulation can—and must—evolve in terms of speed, complexity, and autonomy. As transactions move faster and become more intricate, the potential for systemic risk grows. Autonomous agents, executing financial logic at scale, can amplify shocks or interact in unpredictable ways, creating conditions that existing institution-focused oversight was never designed to handle.

High-frequency agentic flows remove human bottlenecks, allowing hundreds or thousands of micro-transactions to execute instantly. Legacy infrastructure, optimized for human speed and conventional fraud detection, struggles to capture these flows. Without new oversight models, opacity and complexity multiply: thousands of automated payments can become effectively invisible, and AI-driven explanations of outcomes may mislead as easily as they clarify. In this environment, traditional rules tied to entities, licences, or fixed reporting schedules cannot adequately contain risk.

The solution lies in adaptive, data-centric regulation. Oversight must shift from auditing institutions to monitoring protocols and systems. Compliance can be embedded into code, while real-time data enables regulators to track activity, identify anomalies, and enforce accountability continuously. This “internet-native” approach, articulated in 2014 by Union Square Ventures’s Nick Grossman as Regulation, the Internet Way, emphasises open standards, transparency by design, and traceable accountability. Regulators audit the functioning of systems rather than checking static ledgers or relying on delayed reports. And, in initiatives such as the Regulatory Genome Project and its commercial offshoot, RegGenome (another Aperture portfolio company), we start to see the emergence of the infrastructure to make this possible. RegGenome provides granular, traceable and machine-readable data across regulatory themes and disciplines that can be ingested by downstream applications to automate compliance (e.g. Finspector which can systematically check whether financial promotions are compliant with relevant regulations).

Tokenization and programmable payments further support this model, though the principle extends beyond any single technology. By embedding rules into infrastructure and tracking every transaction automatically, regulators gain visibility without restricting innovation. Risk is managed not by limiting participation through upfront permission, but by making all activity traceable and auditable in real time. This allows high-volume, complex, or autonomous flows to scale safely.

The shift mirrors a move from industrial-era supervision to digital-era oversight. Traditional regulation (1.0, in Nick’s framework) resembled inspecting a factory once a year, relying on blueprints and licences. Adaptive regulation (2.0) is like wiring the factory’s entire production line to a dashboard: regulators see every step in real time, can verify safety and compliance instantly, and respond to unexpected behavior without interrupting operations. As payments become agent-driven and programmable, such continuous, protocol-level oversight will be essential to maintaining trust, stability, and systemic resilience across the financial ecosystem.

Standardisation and Platform Power

Another major consequence of programmable payments is the emergence of platforms that serve and empower users, transforming the payment layer from a utility into the operational backbone of the digital economy. As transactions become automated, high-volume, and programmable, bespoke, company-specific payment solutions give way to a set of universal operators capable of providing seamless interoperability across companies and geographies.

The scale and scope of modern financial flows demand standards. Open protocols and shared frameworks, familiar from the internet (TCP, HTTP, SMTP), allow multiple actors to participate without permission or bespoke integration. Tokenization and autonomous agents make low-value, high-frequency transactions feasible for the first time, while embedding compliance and governance directly into infrastructure. Combined, these innovations reduce friction, enable continuous settlement, and make payments predictable and transparent, laying the foundation for universal operators.

A giant like Stripe illustrates how a centralized platform can scale. By offering composable, API-driven services, it allows businesses of any size to embed payments into products, applications, or services. The platform itself becomes a persistent financial identity, hosting millions of transactions, analysing flows, and generating actionable insights. Users benefit from aggregation: personal payment agents can optimize across multiple counterparties, while businesses can track usage, automate billing, and align revenues with outcomes. With recent acquisitions of Bridge and Privy, Stripe demonstrates that it is alive to the potential to use stablecoin rails to lower costs and speed up settlement, especially for cross-border payments.

We believe the same opportunity exists for Vertical SaaS platforms to become payment systems of intelligence. Whichever partners they work with for payments, they sit in the transaction and data flow, making their application the layer at which agentic transactions are likely to be originated and the layer at which smart contracts between different parties are likely to be organized.

The data generated through these flows becomes a source of competitive advantage. Continuous analysis supports predictive financial planning, the orchestration of all relevant embedded financial services, and intelligent inventory management. Payments are no longer merely transactional; they are intelligent flows, driving decision-making, compliance, and monetization. Tokenization embeds rules in the system, and open data feeds allow regulators and users alike to audit activity, creating transparency and trust without restricting scale.

In this new landscape, control over the payment network confers influence over the broader economy. Platforms that standardise and orchestrate flows act as the nervous system of commerce, connecting buyers, sellers, and intermediaries while continuously generating insights. The rise of these operators signals the final phase of transformation: payments are now programmable, autonomous, and central to value creation, rather than a peripheral utility.

Conclusion: Payments as the Core of the Digital Economy

From their beginnings as high-volume, low-margin plumbing, payment systems are transforming into programmable, agent-driven infrastructure capable of supporting every transaction, large or small, simple or complex. The journey from legacy rails to digital networks illustrates how technology, innovation, and regulation interact to reshape fundamental economic flows.

There are three four consequences of this transformation. First, pricing is liberated: revenue models can now track actual usage, outcomes, and value creation rather than relying on fixed subscriptions or tiers. Second, complexity scales: complex payment flows, such as those related to multi-party supply chains, can be executed automatically, removing costs and intermediaries. Third, the unprecedented systemic risk has to be addressed through adaptive, data-centric regulation, allowing oversight to scale with speed and complexity while maintaining accountability. Third, platforms emerge as central operators, standardising payments, generating insights, and acting as the nervous system of commerce. Together, these forces convert payments from a transactional utility into a dynamic layer underpinning the global economy.

For businesses, this shift opens new opportunities: granular monetisation, flexible financial products, and closer alignment with customer behavior. For users, it promises seamless experiences, automated services, and greater control over financial interactions. And for the economy at large, programmable, interoperable payments enable innovation to scale safely and inclusively, unlocking efficiencies that were previously unattainable.

In short, payments are no longer just a means to move money. In this new landscape, they become a platform for value creation, a medium for insight, and a framework for trust. As the digital economy matures, the firms, technologies, and regulations that harness this layer most effectively will shape the contours of economic life for decades to come.

Subscribe to our newsletter

Join our newsletter to stay up to date on features and releases.